The Smart Saver’s Secret: Mastering the Salary Sacrifice Pension

Have you ever asked a close friend about pensions and later felt like you didn’t understand a word? Honestly, I have experienced that quite a few times. We are all on the same page on wanting to save smart for the future. The clever savers do just that through the salary sacrifice pension. This just might be their single most powerful financial ‘hack’. You basically do the work of supercharging your own pension fund. Therefore, you are at the same time lowering your tax bill. This is the difference between just saving and saving smart.

To be honest, we have to be crystal clear that one cannot help but to figure out a huge benefit behind how this potent operation is done if not done as we lay it out in this article. Apart from breaking down the benefits, we also touch on the changes brought by the future that are going to influence this efficient scheme.

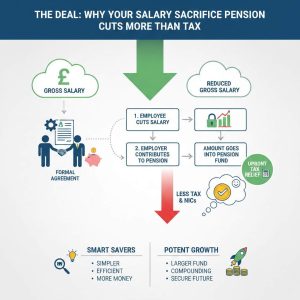

The Deal: Why Your Salary Sacrifice Pension Cuts More Than Tax

What one must do to accomplish a salary sacrifice pension is?

It truly is not hard to understand. The first step is that you get your employer to sign a formal agreement with you. It is agreed that you are to cut your gross (pretax) salary by a certain amount. Most of the time, this particular amount is the one that is equal to your usual pension contribution. The most important step follows immediately, and it is that this amount is put directly into your pension fund. However, as an employer, he/she is now paying that amount. Hence, it is an employer contribution from the legal point of view. The moment which this one-step change caused all the tax advantages of a salary sacrifice pension.

Let us look at it logically for a second. That income of yours which was the base for tax suddenly gets smaller by quite a lot. Tax and National Insurance Contributions (NICs) are both calculated from this new, reduced figure. Thus, the amount of tax paid by you is lowered right away. What is more, one does not have to bother with the quite complicated process of basic rate tax relief claiming from HMRC later. The reason behind all this is that the efficient way of application is made upfront. This efficient process that comes along with a salary sacrifice pension makes it very attractive to all smart savers. They are the ones who are the first to adopt this method if their employer is supportive of it. The use of such a technique as this tool is what makes a your retirement fund the most potent of growth possibilities.

The NICs Advantage: Why this Salary Sacrifice Pension Method is Superior

National Insurance saving is the single biggest financial gain to be made from a salary sacrifice pension.

When you perform the task of a normal pension contribution, the first thing you do is pay NICs.

Then the contribution is deducted from your net pay.

With a salary sacrifice pension situation, the money is not subject to NICs but goes directly to the pension fund. The savings on National Insurance are made both by you and your employer.

Besides, the employer also does not have to pay Employer NICs on the sacrificed amount. Most importantly, the majority of companies will give you a share of the money they have saved. They usually put their NICs savings into your pension pot. This is the main reason why a salary sacrifice pension contribution is extremely powerful. It allows you to keep contributing the same amount. What is more, you are quite often given a bonus top-up from the employer’s NIC savings as well. As a result, your total pension pot grows at a much faster rate. This additional money is, in fact, a little as-if-free cash injection for your future savings. You have to verify if your employer provides this kind of salary sacrifice pension scheme.

Think Twice Before Acting: Income and Other Effects of Salary Sacrifice Pension Plan

The salary sacrifice pension is an efficient tool in a portfolio, yet one has to be aware of the possible hidden drawbacks. Having a lower gross salary may affect certain areas of your life, and these consequences may be quite serious. For example, a decreased salary can possibly influence your capacity to obtain a loan. When counting the income, mortgage lenders usually rely on the gross figure and tips from a different angle. You will probably be able to get smaller loans this way. It is always wise to consult with your lender before going forward.

Besides that, your eligibility to some state benefits might be radically different. Statutory Maternity Pay (SMP) is determined based on your average earnings over a certain period. In case your salary after the sacrifice is too low, the highest SMP rate will correspondingly be exceeded by the maximum rate. Hence, that low-income individuals need to be exceedingly cautious when it comes to a Salary Sacrificing Pension. There should always be a National Minimum Wage level below which your reduced salary must not go for any reason. Also, you need to have a clear understanding of what will happen to those benefits that are linked to your income. This means company life insurance or income protection plans. Often, these policies provide a certain multiple of your lower, post-sacrifice income as pay-out. You need to check the documents of your company’s benefits concerning your salary sacrifice right now.

What’s Next: Changes Coming to the Salary Sacrifice Pension Benefit

We cannot, however, avoid talking about the recent events regarding the salary sacrifice pension and its quite far future. The UK Government has made public that considerable changes are on their way, which will have an effect on the NICs benefit. The modification is aimed solely at the National Insurance advantage that we have talked about earlier.

In fact, the NICs exemption will be soon limited by a fixed cap. As from April 2029, this favor will be officially curtailed. The exemption will be limited to contributions up to the first £2,000 per year. Pension contributions beyond that initial £2,000 limit will be subject to National Insurance charges. This, in turn, will have the most direct impact on the higher-income earners and those who make generous contributions. Nevertheless, the change does not imply terminating the program. It only lessens the advantage of very large contributions and adds some complexity to payroll administration. Therefore, you should still keep working on your salary sacrifice pension plan as your first priority. It is still an excellent vehicle for saving your money in an efficient manner.

Regaining the Power: How to Make the Most of Your Pension Contribution Plan

You are already equipped with information pertaining to the system and main perks. The next step, which would make most sense, is to take immediate action. Delay no more your path to financial freedom and long-term savings. Inquire at your HR office about the availability of an option for salary sacrifice pension plan. Figure out whether they hand the employer NICs savings over to you in the form of a bonus. After that, you may want to consider an online pension contribution tool to plan and calculate your payments more effectively.

Frequently Asked Questions (FAQs)

1. How does a Salary Sacrifice Pension impact my State Pension?

In most cases a Salary Sacrifice Pension does not affect negatively your State Pension. The latter depends on a person’s National Insurance record. If your reduced salary is still above the NIC lower earnings limit, then you are able to keep qualifying years.

2. Should I continue using a Salary Sacrifice Pension even with the 2029 cap?

One should never stop the use of a Salary Sacrifice Pension just because of the existence of the 2029 cap. It is still the best method to save on tax.

3. What is the biggest advantage of a Salary Exchange Pension?

The single most significant feature of a Salary Exchange Pension in comparison with a conventional scheme is the National Insurance saving for both employee and employer. Most of the time, this saving is the reason for a higher net contribution to your pension fund.

4. What are the key checks before starting a Salary Sacrificing Pension?

Before you decide to initiate a Salary Sacrificing Pension operation, it is imperative that you perform checks on four factors: the influence on your mortgage borrowing capacity, the effect on company life assurance cover, the impact on Statutory Maternity/Paternity Pay and whether your salary is still above the National Minimum Wage.

5. Will the upcoming cap affect basic rate taxpayers using a Salary Sacrifice Pension?

The imposing of a cap would be a cause of worry for basic rate taxpayers if and only if their yearly contribution via a Salary Sacrifice Pension was more than £2,000. It is quite possible for a number of basic rate taxpayers to have their contributions currently set at a level that is below the cutting line, which means that the full benefit of the scheme is still available to them.

Share this content:

Post Comment